TARA Risk Reward Looks Favorable

Hello 5C'ers,

TARA Risk Reward Looks Favorable

On Wednesday, I spoke to the CEO of Protara Therapeutics - TARA. This is a very small ($70M MCap), under-the-radar company with a significant catalyst coming in early December 2024. TARA is developing TARA-002, lyophilized, inactivated, genetically distinct Group A Streptococcus pyogenes (similar to a broad immunopotentiator product marketed as Picibanil® in Japan and Taiwan by Chugai Pharma) for the treatment of non-muscle invasive bladder cancer (NMIBC). TARA is developing TARA-002 as an alternative to BCG (Bacillus Calette-Guerin), a live attenuated strain of Mycobacterium bovis, which is used as the front-line therapy in NMIBC but has been under substantial shortage for many years now. However, before TARA-002 can replace BCG, it must first show utility in BCG-unresponsive patients. That's just how the FDA approval process works. There's a second shot on goal in lymphatic malformations, which, if approved, would earn TARA a priority review voucher (PRV), as well as a rare-disease IV Choline product, but for the purpose of this pitch, we're just going to focus on the pending update in NMIBC.

The last time we got news from this program was in April 2024; the data were premature and thus unimpressive. This happens with so many nano-cap biopharma companies. They are so under the radar that they feel the urge to say something to gain attention, but what often happens is what they say is not quite ready to be said, and it ends up killing the stock. What TARA said on April 5th was that the complete response rate (CRR) at 3 months for all 7 BCG-unresponsive patients was 43%. This did not look competitive with other players in this exact population, such as ENGN's (47% CRR at 6 months), CGON (65% at 6 months, 75% any-time up to 6 months), IBRX (63% at 6 months), JNJ (83% any-time). You may have noticed that everyone else has 6 months of data. That's important because responses take time to develop, and releasing data on 7 patients at 3 months perhaps wasn't the wisest decision. Since the April 5th update, TARA's stock is down over 50%.

There's also the nuance of "at 6 months" versus "at any time during the 6 months", with the former clearly the better endpoint for predicting a survival benefit. CRR "at any time during 6 months" doesn't necessarily mean the patient is still in CR at 6 months; it just means, at some point, the tumor disappeared during the first 6 months. So when you see JNJ at 83%, remember they haven't released the "at 6 months" data. You can see that CGON's 6 months of data at 65% is a full 10% below its 75% "any time" data. But getting back to TARA, there's reason to believe that the 6-month update in "at least 10 patients" (per the CEO's guidance) might be much better than the 43% at 3 months they gave us in April. The CEO suggested three reasons for this.

Reason No. 1 is the underlying mechanism of action of TARA-002. Upon intravesical (catheter-based) administration, TARA-002 stimulates innate and adaptive immune responses within the bladder. This activation leads to infiltrating immune cells, such as neutrophils, monocytes, and lymphocytes, into the tumor microenvironment. The activated immune cells secrete various cytokines, including TNF-α, IFN-γ, IL-1β, IL-6, IL-12, and GM-CSF. These cytokines promote a pro-inflammatory response, enhancing the body's ability to target and destroy cancer cells. This inflammatory cascade stimulates an additional anti-tumor immune response that enhances cell lysis. The critical thing to consider here is that the entire process takes time. TARA-002 is not an immediate cytotoxic (chemotherapeutic) agent like gemcitabine or mitomycin. TARA believes efficacy will improve with sustained exposure (maintenance dosing) to TARA-002. There's also the nuance of response by an immunological mechanism, which is more durable than a cytotoxic agent where resistance might develop. This thesis has been proved by long response durations from drugs like Keytruda or cell therapies like TILs. Thus, data at 6 months should be better than at 3 months.

Reason No. 2 is reinduction. Per the protocol, patients who saw a partial response at 3 months were eligible for re-induction dosing (more doses than maintenance dosing). This builds off the explanation of the prior point above.

Reason No. 3 is patient baseline characteristics. The CEO explained that the initial patients enrolled in the study were very late-stage. That's unsurprising; in any initial proof-of-concept study, investigators reserve enrollment for their most sick patients. These are human beings with real diseases, and there are several proven options that patients need to fail before someone is willing to try an unproven option like TARA-002. However, even though the stock dropped 50%, the 3-month data suggests TARA-002 is active. So, TARA has been working with clinical sites in the Phase 1 trial to encourage use in earlier-stage (i.e., healthier) patients. These patients will have more intact immune systems and thus should have stronger immunological responses to TARA-002, as outlined above.

So where does TARA need to be at 6 months? I think, if they can show >55% CRR at 6 months, TARA's stock will be insanely cheap. Remember, ENGN is at 47% CRR at 6 months and has a $400M market cap. CGON is at 65% at 6 months and has a $2.4B market cap. IBRX is at 63% at 6 months (approved) and has a $3.6B market cap.

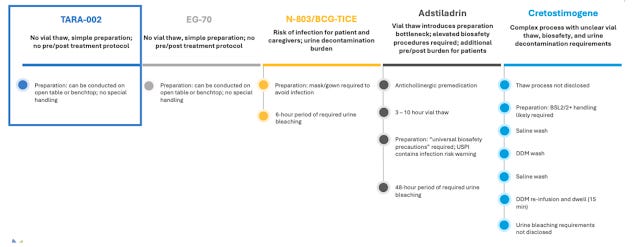

Now, you may be thinking, "Why is 55% at 6 months good for TARA if CGON is at 65%? The answer is dosing! This summary is quickly becoming an opus, so instead of reviewing the significant dosing advantages of TARA-002 compared to CGON, I'll just point you to the slide below. I'm baffled that investors think CGON's product has commercially viable logistics. JNJ's "gemcitabine pretzel" is not shown below, but in my opinion, it also has significant logistic and mechanistic issues.

So, when I look at the slide above, I conclude that if TARA does >55% CRR, that $70M market cap should 5X. In terms of the downside in the stock, I model TARA should exit 2024 with roughly $70M in the bank. Above, I briefly noted the lymphatic malformations and IV Choline products. I think the cash on hand and the potential in lymphatic malformations and with IV Choline should support at least half the current value. So I think TARA has 5X upside and 50% downside, and I think the odds are at least 50/50 (or better) we see a > 55% number in early December 2024 (note: I'm assuming the company releases the data at the Society of Urologic Oncology meeting Dec 6-8, but this has yet to be confirmed). I think that's a bet worth making, so I have a 3% position in the stock.

Cheers,

JNap

PS - Please see important Disclosures/Disclaimers on Bio5C.com

PPS - If you found this post or my research interesting, please consider joining Bio5C. This is an example of an update I send subscribers once or twice a week. You also get a webpage with research on over 100 biopharma stocks, a model portfolio, a ranking of my best ideas, a Discord message board, and a live “Squawk Box” each morning starting at 7AM covering breaking news in the biopharma sector.

PPPS - If you’re not interested in joining but found this post interesting, you can always just buy me a beer » HERE

TARA data looked outstanding today - stock spiked from $3 to $11, then faded hard on fears of an ugly offering. Currently ~$6.